LendVent Income Fund I offers accredited investors an opportunity to invest in a diversified portfolio of high-yielding real estate loans, providing investors with real estate exposure without the typical risks of property ownership.

Our Fund originates, underwrites, and finances loan transactions on high-quality real estate investment properties. The first position real estate collateral of our loans provides inherent security to investors while providing an attractive risk/return balance.

Invest with usTarget Annual Return*

10-14%

Higher yielding / short duration loans are less sensitive to raising rates. The Funds loans are typically 12 months, and no` more than 24 months, with yields north of 10%.

Experience real estate investors are generally unable to access traditional banks for bridge loans. Our Fund has the ability to fill this funding gap, and therefore lend to experienced real estate investors

Conservative loan-to-value underwriting minimizes potential principal losses in the event of a default.

The Fund intends to sell loans in the secondary market to institutional loan buyers and/or replenish the loans through a warehouse facility, enabling the fund to generate a higher yield & mitigate risk.

Loan pool is diversified both geographically as well as by asset class. Risk is spread across entire portfolio

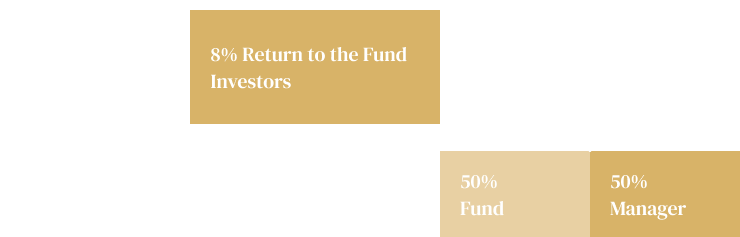

We anticipate that our investors will receive an 10-14% return each year*. The Fund will give payout priority to our investors over the Fund Manager. The Fund Manager receives NO profit sharing until investors have received their 8% Preferred Return.

*Past perfomance does not guarantee future results. Please see the disclaimer page at the end of this presentation for more information.

A non-consumer interest-only mortgage (BPL) secured by real estate investment properties.

Many of the consumer-facing regulations are inapplicable.

Borrower completes application with supporting documents.

Processing collects supporting documents (i.e. PFS, SREO, SOW), pulls credit, conducts background & OFAC search, & orders appraisal

Underwriting reviews all documents, background searches, credit reports, appraisal report, & validates property value

The loan is discussed with the counterparty for a second review & soft approval

Legal dept reviews title, property insurance, entity & other legal documents. Prepares loan documents & ensures compliance

Closing is scheduled and the loan is funded

Florida Office

1160 Kane Concourse, Suite 305

Bal Harbour, FL 33154